Promises, Promises.

Download September Sales and Listings Statistics All Regional

Download September Sales and Listings Statistics Houses Townhouses Condos

Highlights of the September 2024 report

- Bank of Canada should cut its rate by 0.5% this month

- 5th straight month of declining sales in Metro Vancouver

- Highest number of Vancouver condo listings since 2012

- Buy now before everyone else does when the rates come down further

September 2024 brought on promises and more promises. The Bank of Canada dropped their interest rate for the third consecutive time and by the end of the month the U.S. went ahead with their first rate cut – jumping right in with a half point drop. We’re now expecting a half point drop by the Bank of Canada in October based on the latest economic data. And if that wasn’t enough, the province is heading to the polls later in October with promise after promise from the incumbent NDP government and challenging Conservatives. Is it any wonder that buyers are waiting to see what happens? That was the tone of buyers in September, all while sellers jumped back into the market with another rush of listings.

For the third consecutive meeting the Bank of Canada has reduced its key interest rate by a quarter point in September, bringing down mortgage costs for homeowners with variable rate mortgages and lines of credit. While not overly expected, there was some thought that a half point reduction was in order. But what this does now is leave the remaining two meetings open to further reductions in the Bank of Canada’s rate as the economy and inflation numbers clearly indicate that stimulus is needed. Expect both countries to use the remainder of the year to reduce their rates, with Canada going from the current 4.25% to 3.5% or lower by the time 2025 begins.

Many buyers may be thinking that significant Bank of Canada rate cuts will lead to equivalent reductions in fixed rates. But that’s not going to happen. Fixed rates are based on bond yields and current yields have factored in the anticipated drops in the Bank of Canada’s rate. That’s the reason why fixed rates have come down more than 1.5% from their highs already. With economic growth and inflation in Canada lagging, it’s become more likely that the Bank of Canada will cut quicker and deeper than anticipated, so expect variable rate mortgage costs to drop more than fixed rate mortgage costs. That means buyers looking for fixed rate mortgages aren’t going to gain by waiting. With the highest inventory of properties available in the last 6 years, opportunities exist for buyers more so than ever.

There were 1,852 properties sold in Greater Vancouver in September, after 1,903 sold in August, 2,333 properties sold in July, and 2,418 sold in June. With the highest number of active listings available since mid-2019, buyers are still in a holding pattern. Given the path to a sub 3 Bank of Canada rate by some time next year, variable rate mortgages are the flavour of buyers. Taking advantage of the increase in choice will allow those buyers brave enough to buy now and ride the rate down to beat out the competition that will come next spring.

Sales in September were a 4% decrease from the 1,903 properties sold last year, after a 17% decrease in August from the 2,296 properties sold in August 2023. September typically sees a tepid start to the fall market, so less sales in the month after August is not unusual. Will it take another rate cut to further entice more buyers into the market? While the federal government’s promise to extend amortizations for all buyers of presales to 30% and increase of the threshold for insured mortgages to $1.5M gives promise to buyers for easing the mortgage pain, this won’t come until December. Just what the market needs, another reason to wait and push more into the spring market. Buy now or compete later is the mantra of this fall market.

Sales in September were 26% below the 10-year average, like August with sales 26% below the 10-year average after July was 18% below the 10-year average and June was 24% below the 10-year average. The fall market has some work to do to eclipse the spring market in terms of activity but what’s clear is that the longer demand holds off, the busier it will be come the spring. With the inventory of listings continuing to rise, buyers have choice and opportunity like they haven’t seen since 2019.

In Greater Vancouver the number of new listings in September were the highest totals since May after dropping to a low in August. With 6,228 new listings in September, this was a 48% jump from what came on the market in August and an increase of 11% compared to September 2023. Sellers were certainly ready to get into the fall market, even if buyers were still reluctant.

The number of new listings in September were 16% above the 10-year average after August was 1.5% below the 10-year average, July 12% above the 10-year average, and June 2% above the 10-year average. With 3 months left in the year, the total new listings so far are almost at the total for 2023 and will likely be the second highest annual amount in the last 10 years. Even with this, prices had remained relatively flat but are trending lower in the last few months, albeit in the 1 to 3% range for declines. The increase in listings will help keep prices in check as demand enters back into the market at a greater rate over the next year.

There were 14,932 active listings in Greater Vancouver at month end, compared to 13,812 at the end of August, 14,325 at the end of July and 14,180 at the end of June. After being up 46% year-over-year at the end of May, currently there are 31% more active listings year-over-year, a drop from being at 37% at the end of August. While we did see a significant jump in active listings after the month of September, we’re still not at the highs we saw in 2019, although for the month of September we’d have to go back to 2014 to see an active listing count this high for the month of September. Count on total active listings climbing above 15,000 in Greater Vancouver as we move through October before declining through the rest of year.

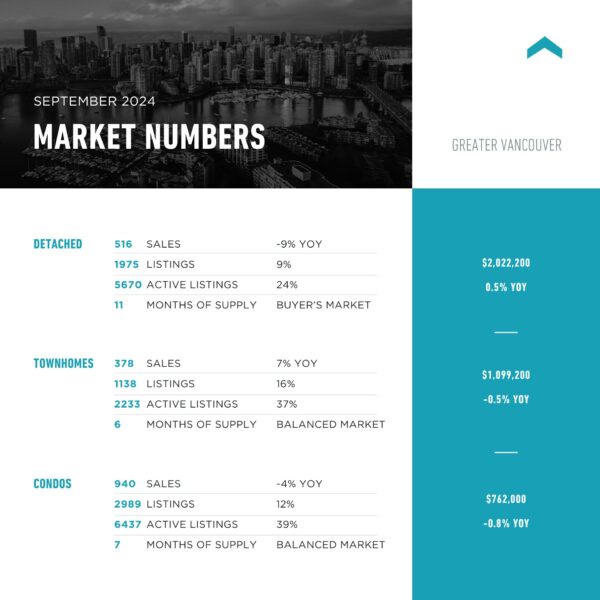

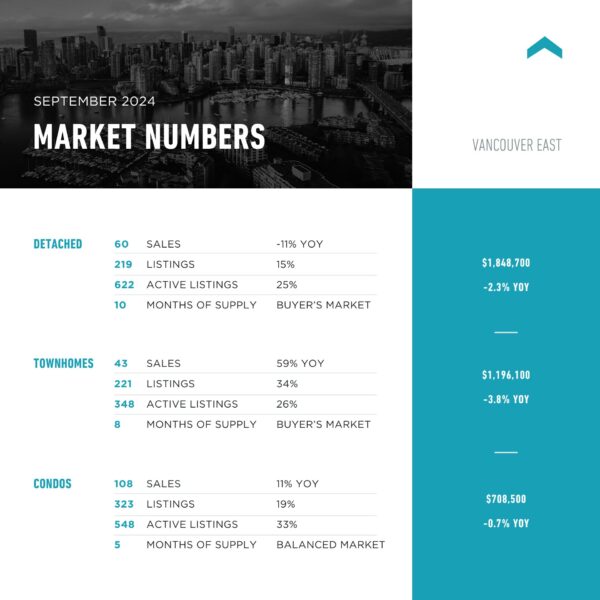

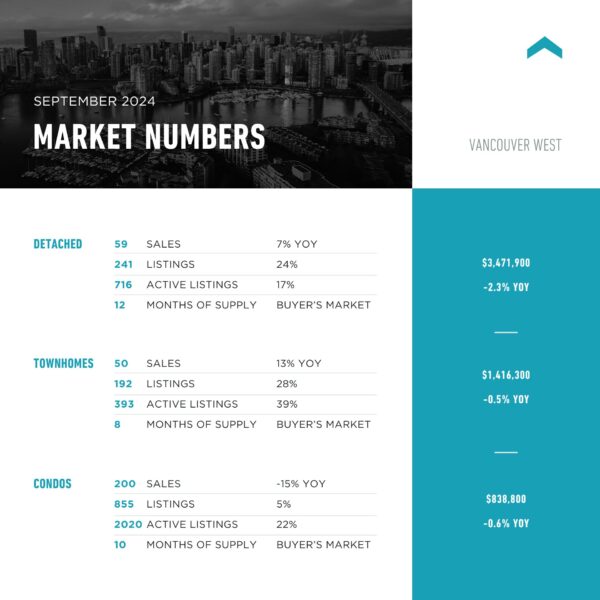

Overall, the detached market in Greater Vancouver is up to 11 months supply from 10 while townhomes remained at 6 months supply and condos climbed to 7 months from 6. Condos have seen the biggest increase in listings with there being 39% active listings year-over-year, with detached at 24% above the same time last year. Detached sales activity has slowed more so though, putting many areas into strong buyer’s markets with over 10 months supply. Vancouver westside condos are at the highest number of active listings since 2012 and sitting with 10 months supply – likely a result of rental legislation and short-term rental rules making that type of property a less attractive investment. Move over to the east side though and sales are up compared to last month and last year with their only being 5 months supply. That’s what a $200,000 difference in average price will do.

As we move through October, election rhetoric and interest rate relief will be a distraction for many buyers. Affordability will continue to be the word thrown around by the two main parties in B.C. when referencing housing, but with so many regulations put in place by the current government, supply suffers at the hands of so many restrictions. Even with the promise to build more, we are still left with the question of how that’s going to happen.

Here’s a summary of the numbers:

Greater Vancouver: Total Units Sold in September were 1,852 – down from 1,903 (3%) in August, down from 2,333 (21%) in July, down from 2,418 (23%) in June, down from 1,93 (4%) in September 2023, up from 1,701 (9%) in September 2022, down from 3,200 (42%) in September 2021, down from 3,741 (50%) in September 2020, and down from 2,363 (22%) in September 2019; Active Listings were at 14,932 at month end compared to 11,382 at that time last year (up 31%) and 13,812 at the end of August (up 8%); the 6,228 New Listings in September were up 48% compared to August 2024, up 14% compared to September 2023, up 43% compared to September 2022, up 17% compared to September 2021, down 6% compared to September 2020, and up 24% compared to September 2019. Month’s supply of total residential listings is up to 8 month’s supply from 7 (buyer’s market conditions) and sales to listings ratio of 30% compared to 45% in August 2024, 35% in September 2023, and 39% in September 2022.

Month-over-month, the house price index is down 1.4% and in the last 6 months down 1.6%.

Vancouver Westside: Total Units Sold in September were 312 – down from 337 (7%) in August, down from 416 (25%) in July, down from 470 (34%) in June, down from 338 (8%) in September 2023, up from 301 (4%) in September 2022, down from 567 (45%) in September 2021, down from 539 (42%) in September 2020, and down from 404 (23%) in September 2019; Active Listings were at 3,174 at month end compared to 2,558 at that time last year (up 24%) and 2,873 at the end of August (up 10%); the 1,302 New Listings in September were up 69% compared to August 2024, up 57% compared to September 2023, up 43% compared to September 2022, up 5% compared to September 2021, down 4% compared to September 2020, and up 31% compared to September 2019. Month’s supply of total residential listings is up to 10 month’s supply from 9 (buyer’s market conditions) and sales to listings ratio of 24% compared to 44% in August 2024, 29% in September 2023, and 33% in September 2022.

Month-over-month, the house price index is down 1.2% and in the last 6 months up 0.4%.

Vancouver East Side: Total Units Sold in September were 211 – up from 193 (9%) in August, down from 263 (20%) in July, down from 270 (22%) in June, up from 192 (10%) in September 2023, up from 178 (19%) in September 2022, down from 368 (43%) in September 2021, down from 443 (52%) in September 2020, and down from 293 (28%) in September 2019; Active Listings were at 1,529 at month end compared to 1,196 at that time last year (up 27%) and 1,407 at the end of August (up 8%); the 772 New Listings in September were up 67% compared to August 2024, up 22% compared to September 2023, up 71% compared to September 2022, up 22% compared to September 2021, down 7% compared to September 2020, and up 33% compared to September 2019. Month’s supply of total residential listings is steady at 7 month’s supply (balanced market conditions) and sales to listings ratio of 28% compared to 42% in August 2024, 31% in September 2023, and 40% in September 2022.

Month-over-month, the house price index is down 1.3% and in the last 6 months down 0.4%.

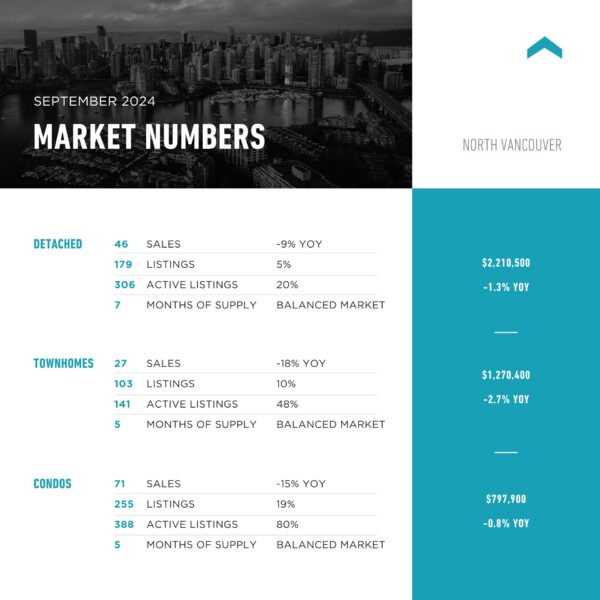

North Vancouver: Total Units Sold in September were 144 – down from 145 (1%) in August, down from 201 (28%) in July, down from 221 (35%) in June, down from 169 (15%) in September 2023, up from 128 (13%) in September 2022, down from 230 (37%) in September 2021, down from 328 (56%) in September 2020, and down from 166 (13%) in September 2019; Active Listings were at 856 at month end compared to 627 at that time last year (up 36%) and 675 at the end of August (up 27%); the 543 New Listings in September were up 102% compared to August 2024, up 13% compared to September 2023, up 35% compared to September 2022, up 29% compared to September 2021, down 8% compared to September 2020, and up 21% compared to September 2019. Month’s supply of total residential listings is up to 6 month’s supply from 5 (balanced market conditions) and sales to listings ratio of 27% compared to 54% in August 2024, 35% in September 2023, and 32% in September 2022.

Month-over-month, the house price index is down 2.5% and in the last 6 months down 3.1%.

West Vancouver: Total Units Sold in September were 45 – down from 57 (21%) in August, down from 59 (24%) in July, down from 75 (40%) in June, down from 53 (15%) in September 2023, up from 42 (7%) in September 2022, down from 71 (37%) in September 2021, down from 98 (54%) in September 2020, and down from 51 (12%) in September 2019; Active Listings were at 724 at month end compared to 626 at that time last year (up 31%) and 678 at the end of August (up 8%); the 237 New Listings in September were up 71% compared to August 2024, down 8% compared to September 2023, up 21% compared to September 2022, up 9% compared to September 2021, up 13% compared to September 2020, and up 1% compared to September 2019. Month’s supply of total residential listings is up to 16 month’s supply from 12 (buyer’s market conditions) and sales to listings ratio of 19% compared to 42% in August 2024, 21% in September 2023, and 22% in September 2022.

Month-over-month, the house price index is down 3.0% but in the last 6 months down 2.8%.

Richmond: Total Units Sold in September were 197 – up from 191 (3%) in August, down from 255 (23%) in July, down from 263 (25%) in June, down from 256 (23%) in September 2023, down from 210 (6%) in September 2022, down from 432 (54%) in September 2021, down from 415 (53%) in September 2020, and down from 283 (30%) in September 2019; Active Listings were at 1,736 at month end compared to 1,268 at that time last year (up 37%) and 1,632 at the end of August (up 6%); the 629 New Listings in September were up 16% compared to August 2024, up 4% compared to September 2023, up 35% compared to September 2022, up 0.5% compared to September 2021, down 10% compared to September 2020, and up 12% compared to September 2019. Month’s supply of total residential listings is steady at 9 month’s supply (balanced market conditions) and sales to listings ratio of 31% compared to 35% in August 2024, 43% in September 2023, and 45% in September 2022.

Month-over-month, the house price index is down 1.2% and in the last 6 months down 2.5%.

Burnaby East: Total Units Sold in September were 29 – up from 25 (16%) in August, down from 33 (12%) in July, up from 17 (71%) in June, up from 18 (61%) in September 2023, up from 17 (18%) in September 2022, down from 38 (24%) in September 2021, down from 41 (29%) in September 2020, and up from 22 (32%) in September 2019; Active Listings were at 148 at month end compared to 96 at that time last year (up 54%) and 140 at the end of August (up 6%); the 67 New Listings in September were up 37% compared to August 2024, up 37% compared to September 2023, up 148% compared to September 2022, up 37% compared to September 2021, up 22% compared to September 2020, and up 20% compared to September 2019. Month’s supply of total residential listings is down to 5 month’s supply from 6 (balanced market conditions) and sales to listings ratio of 43% compared to 51% in August 2024, 37% in September 2023, and 63% in September 2022.

Month-over-month, the house price index is down 1.4% and in the last 6 months down 2.4%.

Burnaby North: Total Units Sold in September were 122 – down from 145 (16%) in August, down from 137 (11%) in July, down from 172 (29%) in June, up from 113 (8%) in September 2023, up from 111 (10%) in September 2022, down from 189 (47%) in September 2021, down from 192 (36%) in September 2020, and down from 138 (6%) in September 2019; Active Listings were at 839 at month end compared to 561 at that time last year (up 49%) and 826 at the end of August (up 1%); the 339 New Listings in September were up 15% compared to August 2024, up 11% compared to September 2023, up 73% compared to September 2022, down 12% compared to September 2021, down 3% compared to September 2020, and up 34% compared to September 2019. Month’s supply of total residential listings is up to 7 month’s supply from 6 (balanced market conditions) and sales to listings ratio of 36% compared to 49% in August 2024, 37% in September 2023, and 57% in September 2022.

Month-over-month, the house price index is down 1.5% and in the last 6 months down 2.1%.

Burnaby South: Total Units Sold in September were 114 – up from 112 (2%) in August, down from 140 (19%) in July, down from 135 (16%) in June, down from 126 (10%) in September 2023, up from 96 (19%) in September 2022, down from 183 (38%) in September 2021, down from 173 (34%) in September 2020, and down from 119 (4%) in September 2019; Active Listings were at 694 at month end compared to 518 at that time last year (up 34%) and 634 at the end of August (up 9%); the 332 New Listings in September were up 49% compared to August 2024, up 18% compared to September 2023, up 53% compared to September 2022, up 16% compared to September 2021, down 8% compared to September 2020, and up 42% compared to September 2019. Month’s supply of total residential listings is steady at 6 month’s supply (balanced market conditions) and sales to listings ratio of 35% compared to 51% in August 2024, 45% in September 2023, and 44% in September 2022.

Month-over-month, the house price index is down 3.4% and in the last 6 months down 4.3%.

New Westminster: Total Units Sold in September were 73 – down from 79 (8%) in August, down from 98 (26%) in July, down from 108 (32%) in June, up from 72 (1%) in September 2023, up from 67 (9%) in September 2022, down from 131 (44%) in September 2021, down from 176 (59%) in September 2020, and down from 110 (34%) in September 2019; Active Listings were at 468 at month end compared to 298 at that time last year (up 57%) and 406 at the end of August (up 15%); the 242 New Listings in September were up 69% compared to August 2024, up 39% compared to September 2023, up 40% compared to September 2022, up 3% compared to September 2021, down 24% compared to September 2020, and up 11% compared to September 2019. Month’s supply of total residential listings is up to 6 month’s supply from 5 (balanced market conditions) and sales to listings ratio of 30% compared to 56% in August 2024, 42% in September 2023, and 39% in September 2022.

Month-over-month, the house price index is up 0.6% and in the last 6 months down 0.3%.

Coquitlam: Total Units Sold in September were 155 – down from 171 (9%) in August, down from 178 (13%) in July, down from 189 (18%) in June, down from 170 (9%) in September 2023, up from 142 (9%) in September 2022, down from 247 (37%) in September 2021, down from 307 (50%) in September 2020, and down from 213 (27%) in September 2019; Active Listings were at 1,146 at month end compared to 713 at that time last year (up 61%) and 1,052 at the end of August (up 9%); the 512 New Listings in September were up 22% compared to August 2024, up 15% compared to September 2023, up 58% compared to September 2022, up 43% compared to September 2021, the same as September 2020, and up 34% compared to September 2019. Month’s supply of total residential listings is up to 7 month’s supply from 6 (balanced market conditions) and sales to listings ratio of 30% compared to 41% in August 2024, 38% in September 2023, and 44% in September 2022.

Month-over-month, the house price index is down 1.5% and in the last 6 months down 3.0%.

Port Moody: Total Units Sold in September were 61 – up from 39 (56%) in August, up from 58 (5%) in July, up from 56 (9%) in June, up from 44 (39%) in September 2023, up from 53 (15%) in September 2022, down from 69 (12%) in September 2021, down from 88 (31%) in September 2020, and up from 49 (24%) in September 2019; Active Listings were at 251 at month end compared to 185 at that time last year (up 36%) and 243 at the end of August (up 3%); the 143 New Listings in September were up 59% compared to August 2024, up 38% compared to September 2023, up 61% compared to September 2022, up 46% compared to September 2021, down 14% compared to September 2020, and up 51% compared to September 2019. Month’s supply of total residential listings is down to 4 month’s supply from 6 (seller’s market conditions) and sales to listings ratio of 43% compared to 43% in August 2024, 42% in September 2023, and 60% in September 2022

Month-over-month, the house price index is down 0.7% and in the last 6 months up 2.4%.

Port Coquitlam: Total Units Sold in September were 52 – down from 56 (7%) in August, down from 66 (21%) in July, down from 62 (16%) in June, down from 65 (20%) in September 2023, up from 50 (4%) in September 2022, down from 97 (46%) in September 2021, down from 114 (54%) in September 2020, and down from 78 (33%) in September 2019; Active Listings were at 358 at month end compared to 191 at that time last year (up 87%) and 306 at the end of August (up 17%); the 186 New Listings in September were up 81% compared to August 2024, up 33% compared to September 2023, up 49% compared to September 2022, up 28% compared to September 2021, down 7% compared to September 2020, and up 28% compared to September 2019. Month’s supply of total residential listings is up to 7 month’s supply from 5 (balanced market conditions) and sales to listings ratio of 28% compared to 55% in August 2024, 47% in September 2023, and 40% in September 2022.

Month-over-month, the house price index is down 2.1% and in the last 6 months down 1.6%.

Pitt Meadows: Total Units Sold in September were 24 – up from 21 (14%) in August, down from 27 (11%) in July, down from 28 (14%) in June, the same as September 2023, up from 20 (20%) in September 2022, down from 41 (41%) in September 2021, down from 44 (45%) in September 2020, and down from 32 (25%) in September 2019; Active Listings were at 125 at month end compared to 94 at that time last year (up 32%) and 105 at the end of August (up 19%); the 70 New Listings in September were up 75% compared to August 2024, up 29% compared to September 2023, up 27% compared to September 2022, up 59% compared to September 2021, down 9% compared to September 2020, and up 19% compared to September 2019. Month’s supply of total residential listings is steady at 5 month’s supply (balanced market conditions) and sales to listings ratio of 34% compared to 52% in August 2024, 44% in September 2023, and 36% in September 2022.

Month-over-month, the house price index is down 1.5% and in the last 6 months down 3.1%.

Maple Ridge: Total Units Sold in September were 114 – down from 123 (7%) in August, down from 166 (31%) in July, down from 130 (12%) in June, up from 108 (6%) in September 2023, down from 115 (1%) in September 2022, down from 182 (37%) in September 2021, down from 267 (57%) in September 2020, and down from 157 (27%) in September 2019; Active Listings were at 887 at month end compared to 752 at that time last year (up 17%) and 855 at the end of August (up 4%); the 344 New Listings in September were up 24% compared to August 2024, down 4% compared to September 2023, up 22% compared to September 2022, up 50% compared to September 2021, up 14% compared to September 2020, and up 21% compared to September 2019. Month’s supply of total residential listings is up to 8 month’s supply from 7 (buyer’s market conditions) and sales to listings ratio of 33% compared to 44% in August 2024, 30% in September 2023, and 40% in September 2022.

Month-over-month, the house price index is down 0.7% and in the last 6 months down 1.2%.

Ladner: Total Units Sold in September were 22 – down from 25 (12%) in August, down from 31 (29%) in July, down from 27 (19%) in June, down from 26 (15%) in September 2023, up from 20 (10%) in September 2022, down from 38 (42%) in September 2021, down from 53 (58%) in September 2020, and down from 28 (21%) in September 2019; Active Listings were at 136 at month end compared to 117 at that time last year (up 16%) and 124 at the end of August (up 10%); the 73 New Listings in September were up 62% compared to August 2024, up 12% compared to September 2023, up 83% compared to September 2022, up 62% compared to September 2021, up 30% compared to September 2020, and up 33% compared to September 2019. Month’s supply of total residential listings is up to 6 month’s supply from 5 (balanced market conditions) and sales to listings ratio of 30% compared to 56% in August 2024, 40% in September 2023, and 50% in September 2022.

Month-over-month, the house price index is up 1.0% and in the last 6 months up 1.6%.

Tsawwassen: Total Units Sold in September were 34 – up from 32 (6%) in August, down from 45 (24%) in July, down from 44 (23%) in June, down from 42 (35%) in September 2023, up from 21 (62%) in September 2022, down from 57 (40%) in September 2021, down from 80 (57%) in September 2020, and up from 26 (31%) in September 2019; Active Listings were at 215 at month end compared to 174 at that time last year (up 23%) and 199 at the end of August (up 7%); the 80 New Listings in September were up 32% compared to August 2024, up 7% compared to September 2023, up 36% compared to September 2022, up 8% compared to September 2021, down 32% compared to September 2020, and the same as September 2019. Month’s supply of total residential listings is steady at 6 month’s supply (buyer’s market conditions) and sales to listings ratio of 43% compared to 53% in August 2024, 57% in September 2023, and 36% in September 2022.

Month-over-month, the house price index is down 2.8% and in the last 6 months down 4.3%.

Fraser Valley: Sales in September were down 8.0%, compared to August and were down 10.7% from September 2023. New listings were up 20.7% from August and up 17.2% from September 2023.The average price was down 2.3% month-over-month and is up 2.4% year-over-year. Active listings were up 4.9% to 9,045 from 8,626 last month and up 38.5% from September 2023 which was at 6,532. Month’s supply of total residential listings is up to 9 month’s supply from 8 (buyer’s market conditions).

“With three rate cuts already and more expected before the end of the year, buyers are watching the market closely to time their purchasing decisions,” said Jeff Chadha, Chair of the Fraser Valley Real Estate Board. “The current conditions should favour buyers, particularly in the detached market, however until we start to see some movement in asking prices, properties will continue to sit on the market for extended periods as both buyers and sellers await the next rate announcement.”

Month-over-month, the house price index is down 1% and in the last 6 months 3%.