Let there be listings

Download Feb Sales and Listings Statistics All Regional

Download Feb Sales and Listings Statistics Houses Townhouses Condos

Highlights of the February 2024 report

- Buyers continue to show up! Number of sales in Greater Vancouver were up 45% from January

- Sellers starting to show up, the number of new listings were up 20% from January

- Bank of Canada continues the holding pattern on its rate – fixed rates declining

- Sales in West Vancouver up 143% compared to January

At the mid-point of February, this month was as much a dark horse to hit 2,000 sales in Greater Vancouver as Billy Mack was to hit the #1 Christmas Song in Love Actually… and like this movie being 20 years old, the sales and new listings amounts feel like they are from 20 years ago. Lack of buyer and seller engagement continues to be one of the significant stories in the market. And as we’ve said before, Metro Vancouver real estate doesn’t have a speculation problem, it has a holding problem. Buyers are holding real estate and not turning into sellers which results in significantly less homes available for other buyers to purchase. But government policy continues to go after the demand side instead of encouraging supply from the existing home stock. Expecting new home construction to fill the void isn’t enough nor realistic.

With the Bank of Canada holding their rate at 5% at the latest meeting this morning, and with the U.S. holding at 5.5% so far this year, the wait continues as to when we might see the first rate cut. The sentiment is that it’s coming. Canadian and U.S. inflation is showing signs of easing, and with the Canadian economy showing signs of weakness, logic would say that rates should be coming down sooner rather than later. Employment numbers remain relatively flat though which isn’t helping in the obvious decision. Canada will likely wait for our neighbours to the south to make the first move, which may come in June when the U.S. has its more in-depth policy decision meeting.

There were 2,070 properties sold in Greater Vancouver in February after, 1,427 properties sold in January this year. This was a 13% increase from the 1,824 properties sold last year in February. Even with one more day in February this year, there were 103.5 sales per day compared to 96 sales per day last year. So, we can’t fully thank the extra day in the leap year for a better February. There is more buyer engagement. The latter half of the month certainly produced more sales, with the last week of the month showing 116 sales per day. A sign the real estate market is continuing to show more activity. This was also the first month where total sales were over 2,000 since August of last year as the fall suffered the fate of two summer interest rate increases by the Bank of Canada. Optimism is gaining in the market as buyers simply need to move on – literally.

With this increase in activity, sales in February were 23% below the 10-year average, after sales in January were 22% below the 10-year average with sales in December 37% below the 10-year average and November’s sales at 35% below the 10-year average. We’re still within a slower moving market, and with a few more listings coming on this month, buyers were given opportunity. And moving forward, they should take advantage of it. February isn’t traditionally a strong month for sales, so expect March to produce more sales, even with spring break in the middle of it.

With the increase sales, we saw a drop to 5 months supply of homes overall in Greater Vancouver, falling back from 6 months in January and 7 months supply in December. Vancouver’s West Side dropped down to 6 months supply from 8 in January and Vancouver’s East Side declined to 4 months (a technical seller’s market) from 6 months in January. Vancouver saw fewer new listings in February compared to other areas of the region, while sales were up 53% compared to January on the West Side and 52% on the East Side. West Vancouver produced twice as many sales in February, bringing months supply down to 9 from 21. Detached sales in each of these cities showing more growth than the other sectors, signalling the upper end of the market is coming back perhaps. The perpetually under supplied North Vancouver dropped down to 3 months supply with condos there at 2 months supply. Further east, Burnaby and beyond have 4 months supply of homes available, with the Tri-Cities down to 3 months supply. Maple Ridge is the anomaly with 5 months supply after significant increase in new listings – up 92% compared to February last year and to 54% compared to January. Active listing counts are up 47% compared to this time last year. Buyers, Maple Ridge is where the opportunities are!

Even with the extra day in the month, we only saw 4,651 new listings in Greater Vancouver. This was well above last year’s total of 3,559 new listings, so that’s a good sign that sellers are coming back, perhaps in response to an uptick in buyer activity. Multiple offers have been occurring in the market more than last fall, an encouraging sign for those sellers that were afraid to enter a quiet market

The challenge of giving up lower mortgage rates continues for many homeowners through, unwilling to enter a higher mortgage rate to make a move. As renewals begin over the next few months and years and as rates start to come down, we’ll see this pent-up supply start to release more into the market. For some sellers, it may be better to take advantage of a lack of listings now and come on the market and work with a mortgage professional to find the right rate for now in anticipation of lower rates in the next few years. Date the rate and marry the house as they say.

The number of new listings in January were right at the 10-year average, which is an improvement from January where they were 13% below the average and December with the number of new listings in that month being 25% below the 10-year average.

There were 9,634 active listings in Greater Vancouver at month end, after there being 8,633 active listings in Greater Vancouver at the end of January and 8,283 at the end of February 2023. The detached market overall has come down to 6 months supply from 8, putting it into balanced market territory. Townhomes remain at 4 months supply and condos dropped to 4 months supply from 5 – putting both into seller market conditions. Depending on price point and area though, some may be more in balanced market conditions. Absorption rates for detached were 39% for the month while townhouses and condos were at 48% and 47% respectively. All segments saw lower absorption rates compared to last year in February, because of more new listings this year. As a result, we are seeing a gain in the active listing counts. This could bring more buyers to the market, again, a good sign for sellers.

Will March be the lion or the lamb in the real estate market. With a sizable increase in both sales and new listings in February compared to the previous month, will March continue down that path. After the provincial budget was announced, buyers and sellers will continue to navigate an incredible amount of policy changes by government, with an anti-flipping tax of 20% to start in 2025 introduced by the BC NDP. The likely effect of this in the years to come will be a reduced number of listings as sellers hold on to properties more than they already are. Perhaps we’ll see a push to sell before 2024 ends though. Increased thresholds for the Property Transfer Tax exemptions starting April 1st will help those buyers purchasing up to $835,000 for resale and up to $1.1 million for newly constructed homes. The first-time homebuyer incentive has been discontinued at the federal level, much to the dismay of Dawson Creek which was the only region of B.C. where the program worked. Goodbye to bad legislation. Unfortunately, that was not the same for the Foreign Buyer Ban as the Federal Liberals announced a further two-year extension on that program which will now run until the end of 2026. All of which do not help but hinder supply of homes, which is the biggest challenge in the housing market, ironically identified by the government too. Too bad policy doesn’t align with reality.

Here’s a summary of the numbers:

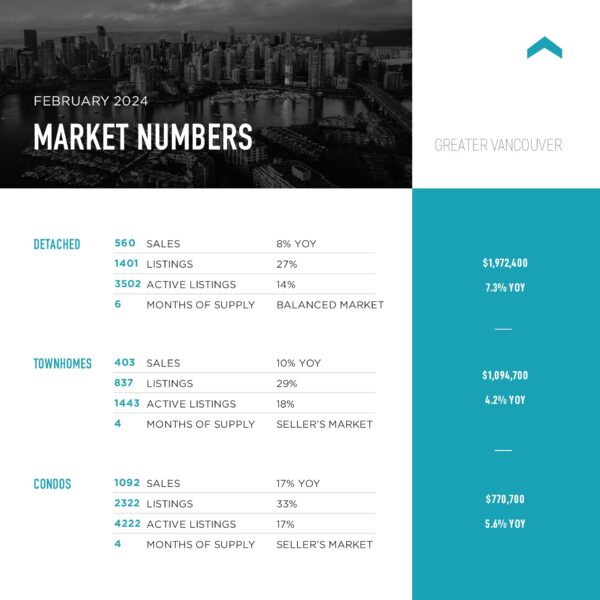

Greater Vancouver: Total Units Sold in February were 2,070 – up from 1,427 (45%) in January, up from 1,345 (54%) in December up from 1,824 (13%) in February 2023, down from 3,451 (40%) in February 2022, down from 3,852 (47%) in February 2021, down from 2,185 (5%) in February 2020, up from 1,512 (40%) in February 2019; Active Listings were at 9,634 at month end compared to 8,283 at that time last year and 8,633 at the end of January; New Listings in February were up 20% compared to January 2024, up 9% compared to February 2023, down 10% compared to February 2022, down 10% compared to February 2021, up 13% compared to February 2020, and up 17% compared to February 2019. Month’s supply of total residential listings is down to 5 month’s supply (balanced market conditions) and sales to listings ratio of 45% compared to 37% in January 2024, 51% in February 2023, 62% in February 2022, and 38% in February 2019. Month-over-month, the house price index is up 1.9% and in the last 6 months down 2.1%. Prices appear to be on the upswing after several months of seeing them decline through the fall.

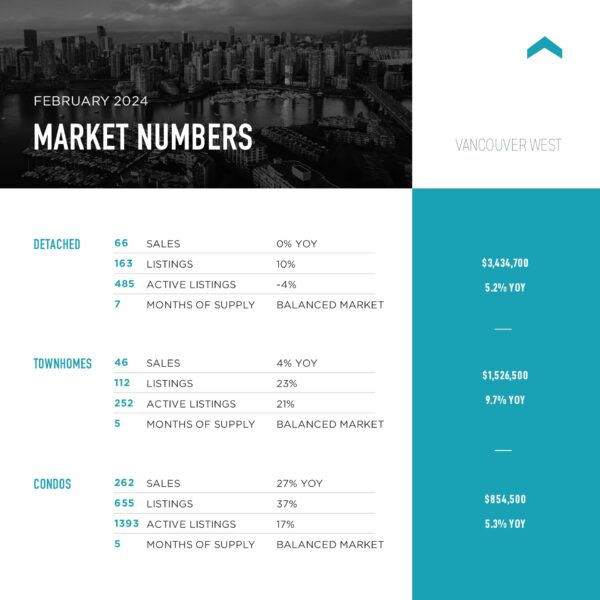

Vancouver Westside: Total Units Sold in February were 374 – up from 245 (53%) in January, up from 235 (59%) in December up from 316 (18%) in February 2023, down from 665 (44%) in February 2022, down from 592 (37%) in February 2021, up from 367 (2%) in February 2020, up from 254 (47%) in February 2019; Active Listings were at 2,148 at month end compared to 1,923 at that time last year and 1,963 at the end of January; New Listings in February were up 10% compared to January 2024, up 31% compared to February 2023, down 15% compared to February 2022, down 1% compared to February 2021, up 32% compared to February 2020, and up 5% compared to February 2019. Month’s supply of total residential listings is down to 6 month’s supply (balanced market conditions) and sales to listings ratio of 40% compared to 29% in January 2024, 44% in February 2023, 61% in February 2022, and 29% in February 2019. Month-over-month, the house price index is up 4.0% and in the last 6 months down 0.7%.

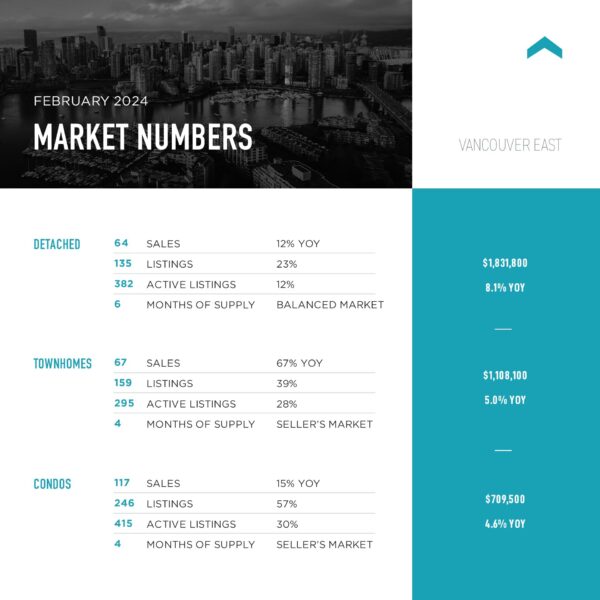

Vancouver East Side: Total Units Sold in February were 249 – up from 164 (52%) in January, up from 148 (68%) in December up from 198 (26%) in February 2023, down from 359 (31%) in February 2022, down from 408 (39%) in February 2021, up from 243 (2%) in February 2020, up from 166 (50%) in February 2019; Active Listings were at 1,109 at month end compared to 900 at that time last year and 990 at the end of January; New Listings in February were up 9% compared to January 2024, up 43% compared to February 2023, down 16% compared to February 2022, down 6% compared to February 2021, up 23% compared to February 2020, and up 41% compared to February 2019. Month’s supply of total residential listings is down to 4 month’s supply (seller’s market conditions) and sales to listings ratio of 46% compared to 33% in January 2024, 52% in February 2023, 55% in February 2022, and 43% in February 2019. Month-over-month, the house price index is up 0.8% and in the last 6 months down 3.5%.

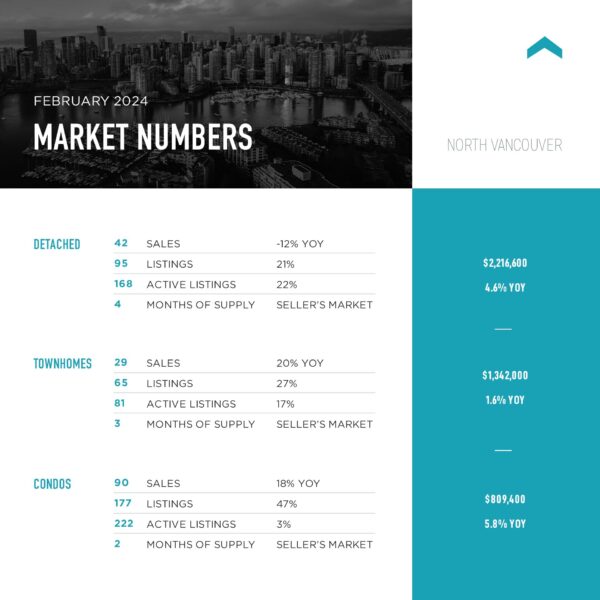

North Vancouver: Total Units Sold in February were 163 – up from 117 (39%) in January, up from 106 (52%) in December up from 1,824 (9%) in February 2023, down from 261 (38%) in February 2022, down from 318 (49%) in February 2021, down from 206 (21%) in February 2020, up from 124 (31%) in February 2019; Active Listings were at 489 at month end compared to 436 at that time last year and 414 at the end of January; New Listings in February were up 27% compared to January 2024, up 35% compared to February 2023, down 16% compared to February 2022, down 20% compared to February 2021, down 8% compared to February 2020, and up 2% compared to February 2019. Month’s supply of total residential listings is down to 3 month’s supply (seller’s market conditions) and sales to listings ratio of 48% compared to 43% in January 2024, 59% in February 2023, 64% in February 2022, and 37% in February 2019. Month-over-month, the house price index is up 1.5% and in the last 6 months down 1.8%.

West Vancouver: Total Units Sold in February were 56 – up from 23 (143%) in January, up from 41 (37%) in December up from 43 (30%) in February 2023, down from 80 (30%) in February 2022, down from 102 (45%) in February 2021, down from 57 (2%) in February 2020, up from 39 (44%) in February 2019; Active Listings were at 526 at month end compared to 443 at that time last year and 483 at the end of January; New Listings in February were down 5% compared to January 2024, up 11% compared to February 2023, down 21% compared to February 2022, up 6% compared to February 2021, up 19% compared to February 2020, and up 1% compared to February 2019. Month’s supply of total residential listings is down to 9 month’s supply from 21 in January (still buyer’s market conditions) and sales to listings ratio of 33% compared to 13% in January 2024, 28% in February 2023, 37% in February 2022, and 23% in February 2019. Month-over-month, the house price index is down 3.7% and in the last 6 months down 6.3%.

Richmond: Total Units Sold in February were 231 – up from 161 (43%) in January, up from 169 (37%) in December up from 227 (2%) in February 2023, down from 340 (30%) in February 2022, down from 453 (49%) in February 2021, down from 253 (9%) in February 2020, up from 155 (49%) in February 2019; Active Listings were at 1,088 at month end compared to 1,036 at that time last year and 1,014 at the end of January; New Listings in February were up 13% compared to January 2024, up 1% compared to February 2023, down 34% compared to February 2022, down 30% compared to February 2021, down 8% compared to February 2020, and down 2% compared to February 2019. Month’s supply of total residential listings is down to 5 month’s supply (balanced market conditions) and sales to listings ratio of 50% compared to 39% in January 2024, 49% in February 2023, 56% in February 2022, and 33% in February 2019. Month-over-month, the house price index is up 2.9% and in the last 6 months down 1.2%.

Burnaby East: Total Units Sold in February were 25 – up from 17 (47%) in January, up from 18 (39%) in December up from 21 (19%) in February 2023, down from 34 (24%) in February 2022, down from 41 (37%) in February 2021, down from 32 (22%) in February 2020, up from 17 (47%) in February 2019; Active Listings were at 94 at month end compared to 71 at that time last year and 77 at the end of January; New Listings in February were up 20% compared to January 2024, up 200% compared to February 2023, down 7% compared to February 2022, down 6% compared to February 2021, up 58% compared to February 2020, and up 67% compared to February 2019. Month’s supply of total residential listings is down to 4 month’s supply (seller’s market conditions) and sales to listings ratio of 42% compared to 34% in January 2024, 105% in February 2023, 52% in February 2022, and 47% in February 2019. Month-over-month, the house price index is up 0.2% and in the last 6 months down 2.6%.

Burnaby North: Total Units Sold in February were 121 – up from 88 (38%) in January, up from 91 (33%) in December down from 134 (2%) in February 2023, down from 226 (46%) in February 2022, down from 193 (37%) in February 2021, up from 100 (21%) in February 2020, up from 84 (44%) in February 2019; Active Listings were at 447 at month end compared to 380 at that time last year and 387 at the end of January; New Listings in February were up 35% compared to January 2024, up 22% compared to February 2023, down 20% compared to February 2022, down 6% compared to February 2021, up 29% compared to February 2020, and up 56% compared to February 2019. Month’s supply of total residential listings is steady at 4 month’s supply (seller’s market conditions) and sales to listings ratio of 49% compared to 48% in January 2024, 66% in February 2023, 72% in February 2022, and 53% in February 2019. Month-over-month, the house price index is up 1.6% and in the last 6 months down 1.7%.

Burnaby South: Total Units Sold in February were 109 – up from 102 (7%) in January, up from 79 (38%) in December down from 118 (8%) in February 2023, down from 200 (45%) in February 2022, down from 201 (46%) in February 2021, up from 105 (4%) in February 2020, up from 83 (31%) in February 2019; Active Listings were at 425 at month end compared to 377 at that time last year and 398 at the end of January; New Listings in February were down 2% compared to January 2024, up 1% compared to February 2023, down 27% compared to February 2022, down 23% compared to February 2021, up 9% compared to February 2020, and up 0.5% compared to February 2019. Month’s supply of total residential listings is steady at 4 month’s supply (seller’s market conditions) and sales to listings ratio of 52% compared to 48% in January 2024, 57% in February 2023, 70% in February 2022, and 40% in February 2019. Month-over-month, the house price index is up 1.6% and in the last 6 months down 2.1%.

New Westminster: Total Units Sold in February were 79 – up from 54 (46%) in January, up from 46 (72%) in December up from 66 (20%) in February 2023, down from 159 (50%) in February 2022, down from 164 (52%) in February 2021, down from 90 (12%) in February 2020, up from 63 (25%) in February 2019; Active Listings were at 300 at month end compared to 222 at that time last year and 242 at the end of January; New Listings in February were up 43% compared to January 2024, up 79% compared to February 2023, down 15% compared to February 2022, down 12% compared to February 2021, up 25% compared to February 2020, and up 16% compared to February 2019. Month’s supply of total residential listings is steady at 4 month’s supply (seller’s market conditions) and sales to listings ratio of 41% compared to 40% in January 2024, 62% in February 2023, 70% in February 2022, and 38% in February 2019. Month-over-month, the house price index is up 0.7% and in the last 6 months down 3.1%.

Coquitlam: Total Units Sold in February were 189 – up from 112 (69%) in January, up from 119 (59%) in December up from 158 (20%) in February 2023, down from 264 (28%) in February 2022, down from 322 (41%) in February 2021, down from 196 (4%) in February 2020, up from 134 (41%) in February 2019; Active Listings were at 599 at month end compared to 466 at that time last year and 521 at the end of January; New Listings in February were up 29% compared to January 2024, up 56% compared to February 2023, down 17% compared to February 2022, down 9% compared to February 2021, up 13% compared to February 2020, and up 28% compared to February 2019. Month’s supply of total residential listings is down to 3 month’s supply (seller’s market conditions) and sales to listings ratio of 51% compared to 39% in January 2024, 67% in February 2023, 59% in February 2022, and 46% in February 2019. Month-over-month, the house price index is up 2.4% and in the last 6 months down 1.8%.

Port Moody: Total Units Sold in February were 46 – up from 31 (48%) in January, up from 25 (84%) in December down from 47 (2%) in February 2023, down from 87 (47%) in February 2022, down from 92 (50%) in February 2021, up from 36 (28%) in February 2020, up from 30 (53%) in February 2019; Active Listings were at 131 at month end compared to 200 at that time last year and 122 at the end of January; New Listings in February were up 47% compared to January 2024, down 11% compared to February 2023, down 32% compared to February 2022, down 38% compared to February 2021, down 26% compared to February 2020, and up 1% compared to February 2019. Month’s supply of total residential listings is down to 3 month’s supply (seller’s market conditions) and sales to listings ratio of 57% compared to 55% in January 2024, 52% in February 2023, 73% in February 2022, and 40% in February 2019. Month-over-month, the house price index is up 1.0% and in the last 6 months down 2.2%.

Port Coquitlam: Total Units Sold in February were 64 – up from 43 (49%) in January, up from 36 (78%) in December up from 40 (60%) in February 2023, down from 108 (40%) in February 2022, down from 122 (48%) in February 2021, down from 83 (23%) in February 2020, up from 60 (7%) in February 2019; Active Listings were at 198 at month end compared to 140 at that time last year and 155 at the end of January; New Listings in February were up 104% compared to January 2024, up 71% compared to February 2023, down 3% compared to February 2022, down 13% compared to February 2021, up 17% compared to February 2020, and up 6% compared to February 2019. Month’s supply of total residential listings is down to 3 month’s supply (seller’s market conditions) and sales to listings ratio of 43% compared to 59% in January 2024, 46% in February 2023, 71% in February 2022, and 43% in February 2019. Month-over-month, the house price index is up 3.2% and in the last 6 months down 1.2%.

Pitt Meadows: Total Units Sold in February were 23 – up from 20 (15%) in January, up from 15 (53%) in February 2023, down from 35 (34%) in February 2022, down from 48 (50%) in February 2021, down from 27 (15%) in February 2020, up from 15 (53%) in February 2019; Active Listings were at 64 at month end compared to 62 at that time last year and 57 at the end of January; New Listings in February were up 18% compared to January 2024, up 66% compared to February 2023, down 10% compared to February 2022, down 20% compared to February 2021, down 12% compared to February 2020, and up 10% compared to February 2019. Month’s supply of total residential listings is steady at 3 month’s supply (seller’s market conditions) and sales to listings ratio of 51% compared to 52% in January 2024, 55% in February 2023, 70% in February 2022, and 36% in February 2019. Month-over-month, the house price index is up 2.8% and in the last 6 months down 0.5%.

Maple Ridge: Total Units Sold in February were 145 – up from 106 (37%) in January, up from 129 (12%) in February 2023, down from 224 (35%) in February 2022, down from 292 (50%) in February 2021, down from 177 (18%) in February 2020, up from 100 (45%) in February 2019; Active Listings were at 678 at month end compared to 462 at that time last year and 563 at the end of January; New Listings in February were up 54% compared to January 2024, up 92% compared to February 2023, up 11% compared to February 2022, up 16% compared to February 2021, up 35% compared to February 2020, and up 94% compared to February 2019. Month’s supply of total residential listings is steady at 5 month’s supply (balanced market conditions) and sales to listings ratio of 36% compared to 40% in January 2024, 62% in February 2023, 62% in February 2022, and 48% in February 2019. Month-over-month, the house price index is up 1.1% and in the last 6 months down 3.6%.

Ladner: Total Units Sold in February were 23 – up from 21 (10%) in January, up from 12 (92%) in December down from 27 (15%) in February 2023, down from 26 (12%) in February 2022, down from 61 (63%) in February 2021, down from 36 (36%) in February 2020, up from 20 (15%) in February 2019; Active Listings were at 82 at month end compared to 98 at that time last year and 83 at the end of January; New Listings in February were up 20% compared to January 2024, down 39% compared to February 2023, down 35% compared to February 2022, down 55% compared to February 2021, up 45% compared to February 2020, and up 26% compared to February 2019. Month’s supply of total residential listings is steady at 4 month’s supply (seller’s market conditions) and sales to listings ratio of 62% compared to 46% in January 2024, 44% in February 2023, 46% in February 2022, and 40% in February 2019. Month-over-month, the house price index is up 0.4% and in the last 6 months down 5.0%.

Tsawwassen: Total Units Sold in February were 38 – up from 24 (58%) in January, up from 21 (81%) in December up from 25 (52%) in February 2023, down from 73 (48%) in February 2022, down from 76 (50%) in February 2021, up from 32 (19%) in February 2020, up from 21 (81%) in February 2019; Active Listings were at 156 at month end compared to 146 at that time last year and 139 at the end of January; New Listings in February were up 47% compared to January 2024, up 42% compared to February 2023, down 26% compared to February 2022, down 27% compared to February 2021, up 39% compared to February 2020, and up 36% compared to February 2019. Month’s supply of total residential listings is down to 4 month’s supply (seller’s market conditions) and sales to listings ratio of 51% compared to 47% in January 2024, 47% in February 2023, 72% in February 2022, and 38% in February 2019. Month-over-month, the house price index is up 0.7% and in the last 6 months down 1.4%.

Fraser Valley: Sales in February were up 32% from January and up 38% from February 2023. New listings were up 18% from January and up 44% from February 2023. While the average price was down 0.1% month-over-month, it is up 8% year-over-year. Active listings were up 14% to 5,561 from 4,877 last month but up 26% from February 2023. After seeing steep declines, active listing counts in the region are climbing. It was a very precipitous decline over the last 3 months. Month-over-month, the house price index is up 0.9% and in the last 6 months down 4.2%.

“There is somewhat of a buzz in the market right now,” said Narinder Bains, Chair of the Fraser Valley Real Estate Board. “We are seeing new listings come onto the market and REALTORS® continue to see more traffic at open houses, however buyers are still exercising caution. We aren’t out of the woods just yet, but the signs are pointing to a further increase in activity as we head into spring.”